On Tuesday I had a post about using just about any VISA card to pay for your rental car to give you additional protection over and above from your normal insurance (please read that post to get some background). Today I will review choosing an AMEX card over a VISA card. In a final post this weekend, I will look at the last few options like an AMEX upgrade or a card that offers primary coverage; but for today’s post, this is just a standard AMEX card we are talking about.

Like VISA, almost ANY AMEX will give you protection. Having said that, just about each AMEX has different T&C as to what the exact benefits are for that card so you have to check. For example, depending on the card, coverage covers only cars with a mfg. suggested retail price of $50,000 for the Delta GOLD or PLATINUM or the RESERVE up to $75,000. VISA has no such firm numbers, but still it shows the importance of checking to see if a car is in fact covered (when the link is working as I was doing final checks and got the below):

For us, who are most likely to have Delta AMEX cards, here are some facts. Also, like with VISA, what are the “got ya’s” we need to know about?

#1) Not covered: expensive cars, which means cars with an original manufacturer’s suggested retail price of $50,000 or more when new.

Can you think of how many cars cost more than $50k MSRP? Big got ya!

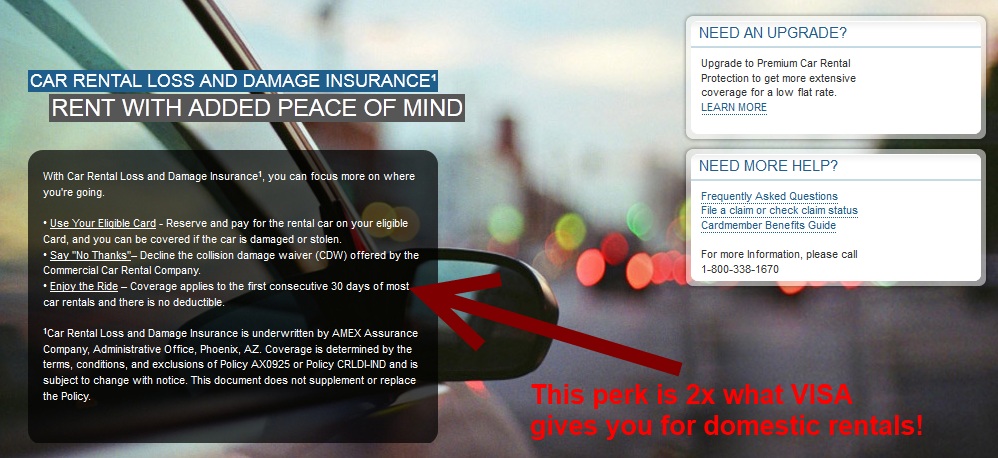

#2) In no event shall coverage be provided when the Card member rents a Rental Auto beyond 30 consecutive days from the same Rental Company, regardless of whether the original agreement is extended, or a new written agreement is entered into, or a new vehicle is rented. Additionally, no coverage will be provided when the Primary Renter rents a Rental Auto for more than 30 consecutive days out of a 45 day period within the same geographic market/location (75 mile radius).

The PRO over VISA is you get 30 days NOT just 15 of coverage, but you can not just switch companies after the time is up. You could go Visa then AMEX then VISA I would think.

#3) NOT COVERED: Full sized sport utility vehicles, including but not limited to, Chevrolet/GMC Suburban, Tahoe and Yukon, Ford Expedition, Lincoln Navigator, Toyota Land Cruiser, Lexus LX450, Range Rover or full-sized Ford Bronco. [also trucks]

YIKES! Many of these are covered with VISA. My last rental in Salt Lake, had I paid with my Delta Reserve card, would NOT have been covered!

#4) No coverage for Australia, Ireland, Israel, Italy, Jamaica, and New Zealand.

Again, you have to check, that is one of the most frustrating things as depending on your card, these terms may or may not be there.

#5) Membership Rewards redemption certificate, in which case, the participating Car Rental Companies mean Hertz, National and Budget, only.

With American Express Membership Reward points, you can see you are limited to only a few car rental companies. There is a clear advantage with Chase Ultimate Rewards®, as you can use them with many more rental car companies.

I could really go on and on with the “got ya’s” like the fact that if your statement is past due you will not be covered but there are exceptions in some states to that. Also, you have to pay for the rental in full so don’t use say 1/2 Ultimate Rewards points and 1/2 AMEX to pay. The bottom line on these is you must read with the card you have just what your perks are and are not. This is one of the hardest parts about this post as there is no way to cover all the points as they are different over infinite circumstances. The same thing goes for Mastercard. You have to check with each card. Some have NO coverage some have similar to VISA or AMEX. So, you just have to check.

To be fair, there are some big things that are perks over VISA like personal property in a car up to $1000 and up $2000 with others in the car. There is life insurance up to $200,000 plus $20,000 per passenger. If you check you will find some others. But for me, the “legalese” and differing conditions for differing cards, even inside the Delta family of cards, really bothers me. To me, the perks of this program do not outweigh the drawbacks. To me, VISA is simple and straight forward across all the VISA products.

Some final personal thoughts. What are you trying to get? Do you want your deductible covered if you have an accident? That is what I am looking for. I am not looking for extra coverage in case of damage to my stuff. I have life insurance so I don’t pay with my AMEX to protect my family if I were to die in a wreck (would they even know to check for this?)! I have never rented a car for more than two weeks, but others I know do. I love so much of what AMEX offers with Delta, but when it comes to this perk, I will NOT have “peace of mind” if I were to choose AMEX to pay for the rental.

So what do you think. Are you surprised by this information? Let me know and check back on Saturday for the final post on this topic! – René

See the FINAL post in this series HERE!

.Editorial Note: Any opinions, analyses, reviews or recommendations expressed in this article are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any card issuer.

▲Delta▲ SkyMiles® Credit Card

RESERVE/PLATINUM/GOLD

from American Express®

Click here for more information

![]()

Responses are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.

anyone actually try making a claim?

@ ЖенЯ – Lucky from One Mile at a Time had a great and perfect result using his AMEX in Germany and getting payment for an accident.

What we need to hear is real life examples of when people used Visa and Amex cards for a rental and were in an accident, and how the CC handled the case.

I once used a MasterCard for a rental and tried to get coverage for a break-in (in which only glass was broken and nothing of significant value stolen). It was torture. Hours wait on hold, short hours of operation of the call-in center, rejection, after rejection. They kept stating I needed to claim it on my own auto insurance but at the time I did not own a car and had no auto insurance. I finally gave up and paid the ridiculous overcharged that the rental car company wanted ($450 to replace a passenger window) because it was still not resolved with MasterCard after 2 months and Thrifty sent me to collections. I knew this was there plan to keep denying until I gave up. In the end I sent a letter to the state DA, BBB, and have never and will never use MasterCard again.

I don’t know if Visa is better but for other purposes I have always had great customer service from Amex and why I use them for purchases of consumer items like electronics and have been using them for car rentals. I will see what happens if I never need a claim.

@Mark P – I would not use MC for many reasons but thanks for your feedback. I also have had PERFECT success with AMEX purchase warranty related issues. From what I have seen so far, VISA is great about these types of claims but would love REAL WORLD feedback about how it went. On “paper”, so far, a std VISA is the clear winner. But, stay tuned for part 3 soon.

to address point number 4 the only card to cover you in those countrys is a mastercard world i believe

When i log on to the AMEX site, I get this offer for car insurance puchase.

By enrolling, you will automatically be billed $24.95* each time you charge a rental car to your American Express® Card until your enrollment is terminated.

* $17.95 for California residents. This product may not be available in certain states.

What Type of Coverage:

Primary coverage of up to $100,000 for theft and damage to your rental car; Secondary coverage of up to $15,000 for medical expenses

Who this Policy Covers:

Cardmembers and Passengers

How you are Charged:

One flat rate of $24.95 for up to 42 consecutive days (30 days for Washington Cardmembers)

Where Coverage is Available:

Coverage is worldwide (except when renting in Australia, Ireland, Israel, Italy, Jamaica or New Zealand)

I looked at the Terms and Condition, and Item #3 above is not mentioned in the exclusions.

Not sure if it is worth signing up for or using the VISA signature card for car rentals.

@johnny – now now, don’t go posting all the stuff I will have in POST3 this weekend or my post will just be a re-hash of readers comments 😉

I’m with Mark, I don’t own my own car and it’s still almost impossible to suss out what is and isn’t covered by credit card companies for those of us without our own insurance. There are a few cards like the United Mileage Plus that had all sorts of bullet points about Primary Coverage, etc., but who really knows until something happens.

I usually decline their LDW, but purchase liability from the car company since that is where you can really be ruined. Anyone with a better idea on this?

I have carried a Diners Club card just for this purpose. It is one the few cards that is PRIMARY for rental car insurance (but not the only). So it is worth the annual fee to avoid having to use my personal insurance for a rental car accident. But I can’t say how easy they are to deal with – and hopefully won’t ever have to try it out!

@John T – yep, I see how this is going, ah well, my post Saturday will be a recap of reader comments and that is fun too – 🙂

@Delta Points: LOL.

Your readers are smart and well educated 🙂

You know what, Rene. I’m very happy you are laying this out in a consolidated format. On the Disney boards, the issue of car insurance comes up from time to time, and most people don’t know or understand their liabilities or their coverage options. It is nice to have the info listed, so all I need to do is point 🙂

@Chris B. – Txs. Wait till part 3. All those who say “Primary” is so much better, OR, the AMEX paid for one is the best way to go, you are in for a surprise!

@ Well i didnt have any experience but 2 of my friend did, its not crash,

1st Costco Amex purchased insurance from AMEX, he lost the car keys (those key less keys) he had to pick up one from the dealer for that rental, and Amex reimbursed him.

2nd my other friend, had a flat tire, although he had insurance from the rental car, they do not cover flat tire (the tire busted, needed replacement), he rented with Discover, so they cover the cost of new tire and labour

I had a question from the original post:

“What about coverage for the other vehicle(s) and property(ies)?”

Was the answer in this post?

@MichaelP – no I will cover that in the final post this weekend. There are some interesting results to know about! – Rene

I would tend to think that for most Visa and Amex cards, the rental coverage “perk” was never really designed to be a perk….or maybe it was long ago but no long is. Seems like there’s far too many hoops to jump through and too many gotchas for these to be really worth while.

The best bet, in my opinion, would be a card where the rental perk is a key part of the card, not just some obscure benefit that is available on all Visa/Amex branded cards.

Can’t wait for the next post on this. I don’t normally worry about this much because my company’s rental agreement provides LDW as part of the contracted rate, but I’m always looking for ways to protect myself when I head out on my own dime.

A number of years ago I slid into a guardrail in a snowstorm and the rental car’s bumper was dented (to the tune of $1400 in their inflated version of auto body repair). Had rented with a Visa, and at the time didn’t own a car or have other coverage. Visa paid the whole amount, no problem, and with very minimal hassle.

Rented vehicle in CA for a trip to Vegas last week. Paid with AMEX BRG 17.95$ per rental. Accident on I15 in Vegas (additional driver driving and was ticketed – at fault). Rental vehicle damaged and was towed away. Other vehicle was damaged but could be driven. Case opened with AMEX & Enterprise. AMEX has confirmed that they will cover entire cost for damaged vehicle (including Tow, Loss of use etc). Personal insurance to cover liability part (damages to other vehicle). Final decision is still not made on coverage personal insurance will provide.

Great post. Can’t wait for part 3. But as it stands so far, you’ve convinced me to rent with my Capital One VISA instead of my Delta Platinum AmEx.

Just pay the $15 to the car rental company to get the coverage. No fine print 100% walk away protection.

@Helen C

for a one or two day rental I would agree.

I think most of the car rental companies in Asia-Pacific region leverage insurance for their customers. In fact the business competition between Amex and Visa actually benefits more for the customers. Car rental in Bahrain isn’t a different scenario.

@HelenC – I’m trying to rent a car for a 72 hour period (4 calendar days) and the charge is $21.99 per calendar day – the total for the company’s CDW is more than the rental fee! So in this case it’s tempting to rely on the VISA coverage…

I have Premium Car Rental Protection through Am Ex. Whenever I use my Am Ex Platinum Card the flat fee of $15 for the duration of the rental (up to four weeks) provides the primary insurance. I had to file a claim this summer when I backed into a guardrail. It covered everything.

@Wayne – Agree. It is a very nice policy for the cost.

A number of years ago I slid into a guardrail in a snowstorm and the rental car’s bumper was dented (to the tune of $1400 in their inflated version of auto body repair). Had rented with a Visa, and at the time didn’t own a car or have other coverage. Visa paid the whole amount, no problem, and with very minimal hassle.

If you use your Amex to cover vehicle they would have to refund you so anyways your paying out of pocket after damage you might as well put LDW from car rental and save the time!!! And the head ace

I had to use AmEx premium rental insurance from an accident late last year. Primary expenses were medical bills. It’s a nightmare trying to get them cover any expense. They will only cover expenses once every other possible personal insurance has denied them in writing. Extremely frustrating to have to chase all of this down. I think their plan is to tire you out so you will give up